Roofing finance can feel like an overwhelming puzzle for many homeowners, especially when the need for a new roof comes unexpectedly. Did you know that the average roof replacement in the U.S. costs between $8,000 and $15,000, depending on materials and location? That’s a major investment.

So, what are your real options when your roof needs urgent repair or full replacement, but your savings fall short? Can you finance the roof safely without overpaying? More importantly, how do you choose between the many offers from roofing contractors, banks or government programs?

According to industry experts, smart roofing finance isn’t just about getting money fast, it’s about choosing the right plan that protects both your home and your financial future. Thousands of homeowners are now taking advantage of flexible financing programs that offer quick approval, low rates and even energy-efficiency rebates for eco-friendly roofs.

If you’re facing a leaking roof, storm damage, or simply planning an upgrade, this guide will walk you step-by-step through the best ways to fund your new roof, from personal loans and contractor financing to government-backed programs available right here in Florida.

Don’t miss the opportunity to make a smart, stress-free decision that keeps your home secure and your budget under control.

Table of Contents

Understanding Roofing Finance and Why It Matters

Roofing finance is more than a payment plan, it’s the safety net that keeps homeowners from feeling trapped between urgent roof damage and limited savings. In Florida, where strong winds, storms and heavy rain can turn a small leak into a serious problem overnight, being able to finance a new roof or repair isn’t just convenient, it’s essential.

A well-structured financing plan allows you to protect your home immediately instead of waiting for damage to spread. According to the Roofing Industry Alliance for Progress, nearly 58% of U.S. homeowners used some form of roof financing last year to manage repair or replacement costs. In Central Florida, that number is even higher because of frequent weather-related damage and insurance deductible changes.

So, roofing finance matters because it gives control back to the homeowner. It allows you to make smart, timely decisions, guided by professionals who understand both the construction side and the financial process. And when your roof is at stake, waiting is rarely the best option.

At Protect Preserve Roofing, we see every week how the right financing option can help a homeowner save their property from further damage. Some clients finance full roof replacements; others cover insurance deductibles or code upgrades that weren’t included in their policies. Each situation is different, but the goal is always the same: restore your roof quickly and responsibly.

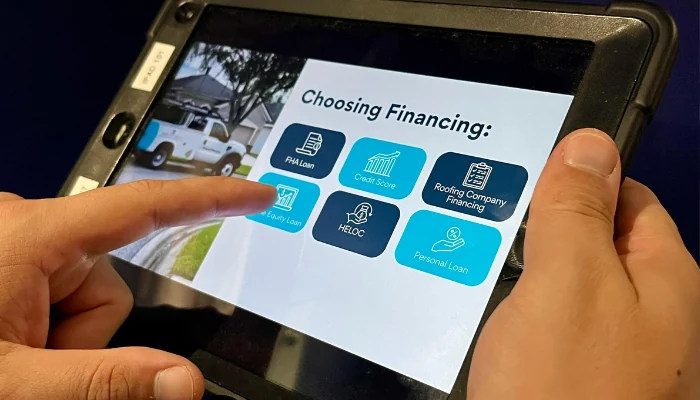

How to Finance a New Roof

Replacing or repairing a roof isn’t cheap, especially in Florida, where materials and labor must meet strict building codes. The good news? You don’t have to pay for everything at once. There are several ways to finance a new roof, and choosing the right one depends on your goals, budget, and how fast you need the work done. Let’s break down the main options.

Home equity loans and HELOCs: Tap into your home’s value

If you’ve built equity in your home, this can be one of the most cost-effective ways to finance a new roof. A home equity loan gives you a fixed amount and a fixed rate, which means predictable monthly payments. A HELOC (Home Equity Line of Credit) works more like a credit card, you borrow what you need, when you need it.

Pros:

- Lower interest rates than most personal loans or credit cards.

- Long repayment terms (10–20 years).

- Interest may be tax-deductible (check with a tax advisor).

Cons:

- Uses your home as collateral.

- Slower approval process than contractor financing.

This option works best for homeowners with solid credit and enough equity to borrow against.

Personal loans: Fast and flexible

When time matters, personal loans can cover your roofing costs quickly. They don’t require collateral and many lenders offer same-week approvals.

Pros:

- No home equity needed.

- Fixed payments and terms.

- Fast funding (some within 24–48 hours).

Cons:

- Higher interest rates than secured loans.

- Shorter repayment terms (usually up to 7 years).

Personal loans are ideal for smaller projects or homeowners who need immediate action but prefer to avoid tapping home equity.

Roofing company financing: Pay over time with trusted contractors

Many licensed roofing companies, like Protect Preserve Roofing, offer in-house financing through lending partners. This option keeps everything simple: one team handles your inspection, repair and payment plan.

Pros:

- Quick approval and easy paperwork.

- “No interest if paid in full within 12–24 months” programs available.

- Payments often start after the job is complete.

Cons:

- Rates and terms vary by lender.

- Financing typically limited to the project cost.

This route is especially useful if you want one point of contact for both the work and the financing. You can learn more or request a quote directly at Protect Preserve Roofing.

Government-backed and FHA title 1 loans: For broader access

If you don’t have much equity or have a limited credit history, you may qualify for FHA Title 1 home improvement loans. These are backed by the Federal Housing Administration and designed for projects like roof replacements.

Pros:

- No equity required for loans under $7,500.

- Fixed interest rates.

- Long repayment terms (up to 20 years).

Cons:

- Requires lender participation.

- Paperwork can take longer.

While these programs aren’t unique to Florida, they’re helpful for homeowners who need affordable financing without risking their home equity.

Credit cards and store financing: Short-term, quick solutions

Retailers such as Home Depot or Lowe’s, and even some banks, offer store credit lines or project cards that can be used for roofing materials or smaller repairs.

Pros:

- Easy approval.

- Promotional rates (0% APR for a few months).

- Useful for emergency repairs or deductibles.

Cons:

- High interest if balance isn’t paid during promotional period.

- Often covers materials, not labor.

These options make sense for short-term fixes or smaller gaps in your financing plan, not for full replacements.

Pro tip from Protect Preserve Roofing: Each of these options helps solve a different problem. Some lower your total cost; others get the job started faster. In Florida’s unpredictable weather, the key is timing, acting before the next storm, not after.

Comparing Roof Financing Options Side by Side

In Florida, weather damage can’t wait, but your wallet might need some flexibility. Below is a straightforward comparison of the main roofing finance options homeowners use to protect their homes without delay.

| Financing Option | Best For | Typical Interest Rate | Approval Speed | Repayment Term | Collateral Needed | Key Benefits | Considerations |

| Home Equity Loan | Homeowners with solid equity and strong credit | 6%–9% (fixed) | 1–3 weeks | 10–20 years | Yes – your home | Lowest long-term rates, fixed monthly payments | Longer process, home used as collateral |

| HELOC (Home Equity Line of Credit) | Homeowners planning ongoing projects | Starts around 7% (variable) | 1–2 weeks | Up to 20 years | Yes – your home | Flexible withdrawals, reuse credit as needed | Rates can increase, variable payments |

| Personal Loan | Quick roof replacement after storm damage | 8%–15% (fixed) | 1–5 days | 2–7 years | No | Fast approval, no equity required | Higher interest, shorter terms |

| Roofing Company Financing | Homeowners wanting everything handled by one team | 0%–14.99% (promotional or fixed) | Same day–3 days | 1–10 years | No | Easy setup, fast approval, “No Interest if Paid in Full” offers | Limited to project total, rates vary |

| FHA Title 1 Loan | Limited credit or low home equity | 6%–10% (fixed) | 2–4 weeks | Up to 20 years | No (under $7,500) | Government-backed, long repayment window | More paperwork, slower processing |

| Credit Card / Store Financing | Small repairs or deductible coverage | 0%–24% (promo or standard) | Same day | 6–24 months | No | Fast approval, promotional 0% APR options | High interest after promo, usually materials only |

Real-world example:

A homeowner in Orlando recently financed a full shingle roof replacement through contractor financing, getting same-day approval with a 0% interest plan for 18 months. Another client in Daytona Beach used a HELOC to fund a long-term metal roof upgrade, locking in a lower rate and extending payments over 15 years.

Each option has its place.

- If you need the lowest rate, a home equity loan or HELOC is best.

- If you need speed, a personal loan or roofing company financing moves faster.

- If your credit or equity is limited, consider FHA Title 1 or short-term promotional credit for quick relief.

At Protect Preserve Roofing, we help you take action without waiting on long bank approvals. You can get started now with a free financing consultation and quote right here: Request Your Estimate

Roof Financing with Local Roofing Contractors

Financing a roof doesn’t have to mean juggling banks, brokers and endless forms. In fact, working directly with a local roofing contractor can be one of the fastest, easiest and most transparent ways to get your roof repaired or replaced, especially here in Orlando and Central Florida, where storms don’t wait for paperwork.

Why local roofing financing works better

Local contractors understand Florida’s unique challenges (hurricane season, humidity and strict building codes). They know how urgent it is to act before water damage spreads. By offering direct roofing finance options, they remove the middlemen and keep the process moving.

Here’s what makes it different:

- Fast Approvals: Many plans are approved the same day.

- Simple Terms: Fixed payments with no hidden surprises.

- Flexible Options: Pay in full later or spread payments over 12–24 months.

- One Point of Contact: The same team that installs your roof handles the financing process, saving time and confusion.

This kind of financing fits perfectly for Florida homeowners facing storm damage or emergency repairs. Instead of waiting weeks for a loan, you can get started right away with confidence your roof will be protected before the next rain hits.

Do roofing companies really offer financing?

Yes. Many do, but not all programs are equal. Some national providers push one-size-fits-all plans that don’t reflect local pricing or codes. That’s where Protect Preserve Roofing stands apart.

We provide roof financing made for Floridians, with terms designed for real-life situations: covering insurance deductibles, code upgrades, or even full replacements. Whether you need a quick repair after a storm or want to upgrade to a stronger shingle or metal system, our financing options make it possible without draining your savings.

Our process is clear, fast and local:

- Free Roof Evaluation: We inspect the roof, document any issues, and give you a detailed estimate.

- Financing Review: You’ll see multiple payment options, some with 0% interest if paid within 12–24 months.

- Project Scheduling: Once approved, work begins immediately, no delays waiting for external approvals.

- Completion & Warranty: You make easy monthly payments while your new roof protects your home for decades.

Quick reminder: Your roof won’t wait for perfect timing and with flexible financing through a trusted Florida contractor, neither should you.

How to Apply and Get Approved Fast

When your roof starts leaking or your shingles begin to lift after a storm, waiting weeks for bank approval isn’t an option. That’s why most Florida homeowners now prefer contractor-based roof financing, it’s faster, simpler and built for real-life emergencies. Here’s how to move from “roof damage” to “approved and scheduled” without the stress.

Step 1. Request a free roofing estimate

Everything starts with a clear inspection. At Protect Preserve Roofing, we provide a no-obligation estimate that includes:

- A visual inspection of your roof’s condition.

- Photos of damage or aging areas.

- A written project scope and repair or replacement options.

This isn’t an insurance inspection, it’s a construction estimate, designed to help you understand what your roof needs and what it will cost to fix it correctly.

Step 2. Choose your financing plan

Once your estimate is ready, you’ll see several financing options from our trusted lending partners. These include:

- 0% interest if paid within 12–24 months.

- Low fixed-rate plans for longer terms (up to 10 years).

- Deferred payments for homeowners managing multiple repairs.

The goal is simple: Give you flexibility to protect your home without financial pressure. You pick the plan that fits your budget and timeline best.

Step 3. Quick application and same-day decision

You can apply online or directly with our team. Approval usually takes minutes, not days. Here’s what you’ll typically need:

- A valid ID.

- Proof of income or employment.

- Your project estimate from Protect Preserve Roofing.

Our partners use soft credit checks whenever possible, so applying won’t hurt your credit score. Once approved, you’ll receive your terms and monthly payment details immediately.

Step 4. Schedule and secure your roof project

After approval, our team schedules your project right away. Most installations or repairs begin within days, long before most traditional lenders would even finish reviewing your paperwork.

You don’t pay a cent until work starts, and you’ll receive complete documentation of your financing agreement for transparency and peace of mind.

Step 5. Enjoy peace of mind under a strong, code-compliant roof

From here, everything runs smoothly. Your roof is installed, your warranty is issued and you make simple, predictable payments while enjoying full protection against Florida’s weather.

The best part? You handled everything in one place, inspection, financing, installation and documentation, without dealing with multiple companies or confusing loan portals.

Ready to start? You can complete the first step in under a minute: Request Your Roofing and Financing Estimate Now.

Your roof shouldn’t wait for approval. With a local Florida partner who handles both the work and the financing, you can move from damage to done fast.

Smart Tips to Save Money When Financing a Roof

Financing a roof doesn’t have to mean spending more, it means spending smarter. The right strategy can help you lock in lower payments, protect your investment and even improve your home’s efficiency over time. Here are practical, Florida-focused ways to save money while financing your roof.

Combine insurance, rebates and financing

If your roof was damaged in a storm, you may be eligible for partial insurance coverage. Even if your insurance doesn’t cover the full replacement, you can combine a payout with roof financing to cover the rest.

Some homeowners also qualify for energy-efficiency rebates or tax credits by upgrading to reflective “cool roof” shingles or metal systems that meet Energy Star® standards.

Example: A homeowner in Tampa Bay used their insurance deductible to cover $2,000, financed $9,500 through Protect Preserve Roofing’s lending partner, and earned a $600 energy rebate, all while paying less than $150/month.

Always keep your insurance receipts and rebate documentation, these can offset costs and reduce your overall project price.

Choose energy-efficient roofing materials

In Florida’s heat, the right material can cut cooling costs by up to 20% annually (U.S. Department of Energy). When comparing materials:

- Cool roof shingles reflect sunlight instead of absorbing it.

- Metal roofs dissipate heat faster than asphalt.

- Tile roofs provide natural insulation for coastal climates.

Even if energy-efficient systems cost more upfront, the long-term savings on utilities and insurance premiums make them a smart financial move.

Avoid temporary fixes that cost more later

A “cheap” or temporary patch often leads to repeated repairs and more financing down the road.

If you’re already taking out a roof loan, use it to do the job right the first time: replace damaged decking, upgrade flashing, and install code-compliant materials.

As we often say at Protect Preserve Roofing, “fast fixes fade fast, quality lasts.”

Maintain your roof to protect your financing investment

Even a brand-new roof needs care. A simple maintenance plan helps you avoid early deterioration and keeps your financing worthwhile.

Schedule professional inspections at least once a year, especially after hurricanes or heavy wind events. Regular checks catch loose shingles, cracked sealants or debris buildup before they turn into leaks.

Our team offers follow-up inspections after every major storm to ensure your roof stays strong year-round.

Watch out for “too-good-to-be-true” financing offers

Some lenders advertise low monthly payments but hide fees or large balloon payments later. Always read the fine print. Look for clear answers to these questions:

- Is the interest rate fixed or variable?

- Are there prepayment penalties?

- Does the rate change after a promotional period?

Consider financing code upgrades or preventive work

Financing isn’t only for full replacements. You can also use it for smaller upgrades that extend your roof’s life, like secondary water barriers, improved ventilation or impact-resistant shingles. These improvements can strengthen your home against future storm damage and may lower future insurance costs.

Take advantage of early payoff options

If you can pay off your loan early, do it. Many financing plans offer “No Interest if Paid in Full within 12–24 months.”

That means you can spread payments out without paying a cent in interest, as long as you clear the balance before the deadline.

Pro tip: Even paying one extra monthly installment can shave months off your financing term.

Quick reminder: Financing your roof the smart way isn’t about cutting corners; it’s about maximizing value. By combining rebates, choosing efficient materials and partnering with a transparent contractor like Protect Preserve Roofing, you can protect your home and your budget at the same time.

Conclusion: Financing That Comes to You

When it comes to roof repairs or replacements, timing is everything. The longer you wait, the higher the risk and the bigger the bill. That’s why Protect Preserve Roofing was built around one simple promise: we come to you, bringing the expertise, materials and financing options right to your doorstep anywhere in Orlando or Central Florida.

We know every situation is different. Maybe your roof was damaged after a summer storm or you’re planning an upgrade before hurricane season. Whatever the reason, we meet you where you are, literally and financially. Our team handles the inspection, project planning and financing process in one visit, so you don’t have to chase multiple companies or lenders.

Here’s what you can expect from us:

- Fast response times: We aim to inspect and quote within 24–48 hours.

- Local expertise: Our crews know Florida roofs, how heat, salt air and storms affect every type of shingle, tile or metal system.

- Flexible financing: Choose from short-term, low-interest or deferred-payment plans.

- Complete transparency: All terms, warranties, and documentation are provided upfront, no hidden fees, no confusing fine print.

The important part is that we believe financing should make your life easier, not harder. Whether you need a repair, a replacement or a full upgrade, we bring solutions directly to your home, so you can protect what matters most without breaking stride.

Live in Orlando or anywhere across Central Florida? Let’s get your roof back in shape and your finances under control.

Start today with a no-obligation roofing and financing estimate with us.

Licensed. Insured. Florida Roofing Experts.

We handle your roof. You stay protected.

Can I really finance a new roof in Florida?

Yes. Many Florida homeowners choose financing instead of paying out of pocket. Whether it’s a full roof replacement, an insurance deductible, or emergency repairs, you can spread payments over time with flexible plans offered through Protect Preserve Roofing and its trusted lending partners.

How fast can I get approved for roof financing?

Most applications are approved within minutes, and work can begin shortly after. For more complex projects, approval may take 1–3 business days. Once you’re approved, we finalize your project schedule immediately to keep your home protected.

Can I use financing if my roof was damaged by a storm?

Yes, as long as the work is for construction and restoration. If insurance covers part of the project, financing can cover the rest. Keep in mind that Protect Preserve Roofing provides construction services only—we don’t negotiate or handle insurance claims.

Why choose a local company like Protect Preserve Roofing?

Because we live and work where you do. We understand Florida’s storms, codes, and insurance requirements better than anyone. Plus, our local financing programs are designed for real-life challenges—fast, flexible, and fair.

Leave a Reply