Does home insurance cover roof shingles or are you stuck paying out of pocket when a storm rips them off? This is the question that keeps many Florida homeowners up at night. According to the National Roofing Contractors Association, asphalt shingles cover over 75% of U.S. homes and yet most owners don’t fully understand what their insurance covers.

Here’s the deal: not every missing or damaged shingle qualifies for a payout. Insurance companies don’t pay just because a few blew off. They look at the cause, the extent of the damage and even how well you’ve maintained your roof over time.

That’s why this guide is different. We’re not here to confuse you with fine print. We’re here to show you exactly when your shingles are covered, how to document damage, what adjusters look for and what you must do now to avoid a denied claim later.

So, let’s break it down with real answers, not insurance lingo.

Table of contents

Does Home Insurance Cover Roof Shingles?

Before we get into it: Shingle roof repairs average $6,000 to $11,000 in the U.S., depending on size, pitch, and material. So, knowing if your insurance steps in can save you a serious headache (and cash). Let’s take a look at:

| Scenario | Does Insurance Cover It? | Why or Why Not? |

| Shingles blown off by strong wind | Yes | Considered sudden damage from a covered peril. Most insurers approve this. |

| Hail cracked or broke shingles | Yes | Hail is usually included in standard policies. Inspection may be required. |

| Tree fell during a storm and broke the roof | Yes | If caused by storm, it’s covered. If the tree was dead and fell without a storm, it might be denied. |

| Roof caught fire | Yes | Fire damage is covered in nearly all policies, no matter the cause. |

| Vandalism to the roof | Yes | Rare, but covered if reported and investigated properly. |

| Shingles cracked from age | No | Age-related wear and tear is the homeowner’s responsibility. |

| Poor roof installation | No | Insurance doesn’t cover contractor mistakes or shortcuts. |

| Neglected maintenance | No | If the roof was already damaged and not fixed, claims are denied. |

| DIY repair gone wrong | No | Homeowner-caused damage isn’t covered unless it leads to other covered events. |

Pro tip from Protect Preserve Roofing: If the damage happened suddenly (like from a storm or a roof leak), insurance may cover it

Wind or Wear? When Insurance Pays for Shingle Damage

When shingles start flying off your roof, your first thought might be, “Will insurance cover this?” But not all shingle damage is created equal, and your insurance company knows it. Let’s break it down clearly so you know where you stand:

| Type of Damage | Insurance Likely Covers It? | Why It Matters |

| Shingles torn off by high winds | Yes | Storm damage is a covered peril in most standard policies. |

| Lifted shingles after a tropical storm | Likely | If damage is recent and from a named storm, you’re in good shape. |

| Shingles cracked from age | No | Gradual deterioration is considered homeowner maintenance. |

| Granule loss from years of sun | No | Normal aging isn’t covered. Time to save for a replacement. |

| Loose shingles from poor installation | No | Faulty workmanship isn’t your insurer’s problem. It’s on the roofer. |

| Shingles lifted but not missing | Maybe | Depends on your policy and the inspector’s judgment. Keep photo proof. |

Keep in mind that to strengthen your wind-damage claim you need:

- Take clear pictures of missing or damaged shingles right after the storm.

- Note the date and time of the storm.

- Keep weather reports or alerts as supporting documents.

- Get a licensed roofer’s inspection (Protect Preserve Roofing does that).

- Be proactive. Don’t wait for leaks to appear, damage might be hidden under the surface.

What Florida homeowners should know

Windstorms are common in Orlando and Central Florida. However, insurers will dig deep to decide if it was the wind or just old age. That’s why a proper inspection can tip the scale in your favor.

Does home insurance cover roof shingles that blew off?

It depends. If your shingles were ripped off by wind, hail or a named storm, you’re likely covered. That’s because most standard homeowner insurance policies protect against “sudden and accidental” damage caused by specific perils. For example:

- High winds during a storm.

- Tropical storms or hurricanes.

- Falling tree limbs caused by weather.

- Hailstorms.

If your roof was in good condition before the storm, you’re in a stronger position to get your claim approved. On the flip side, if the damage happened over time, or your roof was already looking tired, you might be out of luck.

- Old or worn shingles.

- Damage from poor maintenance.

- Pre-existing issues.

- Improper installation.

Insurance companies are picky. If the inspector thinks the roof was neglected or already failing, they’ll likely deny the claim.

Pro tip from Protect Preserve Roofing: Here are a few smart moves to help you get a “yes” instead of a “no”:

- Get a written inspection from a licensed roofer.

- Photograph the damage immediately, don’t wait!

- Document the date of the storm using local weather data.

- Act fast. Most policies have a limited time window to file a claim after the damage.

Florida Homeowners: What You Need to Know About Roof Claims

Living in Florida comes with sunshine, beaches… and the occasional roof-ripping storm. If you own a home here, understanding how roof insurance claims work can save you time, money, and a whole lot of stress.

Not all damage is covered

In Florida, homeowner’s insurance usually covers sudden storm-related damage. That means things like:

- Wind tearing off shingles.

- Hail cracking tiles.

- Fallen tree limbs during a storm.

- Lightning strikes causing roof fires.

But it won’t cover:

- Roofs older than 15–20 years with no updates.

- Wear and tear from sun exposure.

- Mold or rot from long-term leaks.

- Damage caused by neglect or poor maintenance.

If your roof damage is building up slowly, expect the insurer to push back.

Your roof’s age matters

Many Florida insurance policies offer limited or no coverage for roofs over a certain age, especially if they’re made of asphalt shingles. In fact, some insurers are refusing to renew policies for homes with roofs older than 15 years.

Tip: If your roof is getting up there in years, talk to a licensed roofer. A pre-storm inspection can be your insurance policy for your insurance policy.

Documentation is your best friend

When it comes to filing a claim in Florida, proof is power. Be ready to provide:

- Clear photos of the damage.

- Date and time of the storm.

- Any inspection reports you already have.

- Maintenance history, if available.

These details help show the damage wasn’t your fault, it was the storm’s.

Your insurance adjuster isn’t a roofer

Adjusters work for insurance companies. Their job? Minimize payouts. That’s why it’s smart to have your own roofer inspect the damage before the adjuster arrives.

If you’re in Orlando or Central Florida, Protect Preserve Roofing sends licensed professionals to help document roof damage and assist during the claim process.

Emergency tarps are often reimbursable

Here’s something most homeowners don’t know: If your roof was damaged in a storm and is leaking, installing an emergency tarp is considered “reasonable prevention”. Many Florida policies will reimburse this cost – as long as you save the receipt and use a licensed roofing company.

And a quick heads-up: never nail or screw a tarp directly into your roof. That can void your claim. Protect Preserve Roofing uses safe methods with sandbags or weighted anchors to avoid extra damage.

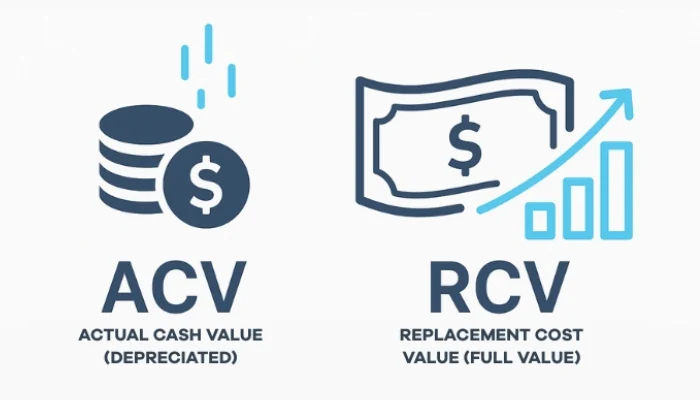

How Much Can You Expect to Receive? (ACV vs. RCV Explained)

Insurance talk can feel like bullshit. Therefore, if your roof is damaged, knowing the difference between ACV and RCV can mean thousands of dollars in or out of your pocket. So, let’s get straight to the point.

First, what do ACV and RCV mean?

| Term | Stands For | What It Means for You |

| ACV | Actual Cash Value | What your roof is worth today, factoring in depreciation. |

| RCV | Replacement Cost Value | What it would cost to fully replace your roof at today’s price. |

One gives you a “used price” and the other covers the price of a new roof.

Florida policies: what’s more common?

In Florida, many insurance companies start with ACV and may reimburse RCV only after you’ve completed the roof replacement and submitted proof. This is called a “recoverable depreciation” policy. It means you:

- Get a first payment based on ACV.

- Fix the roof.

- Send receipts.

- They release the rest (the depreciation value).

How do you know what type you have?

Check your Declarations Page or ask your insurance rep:

- Does my policy pay Actual Cash Value or Replacement Cost?

- If RCV, is depreciation recoverable after repairs?

- Is there a time limit to submit receipts?

Knowing this upfront avoids nasty surprises later.

Quick reminder: Want someone to walk through your policy with you? Our team at Protect Preserve Roofing is just a call away and yes, we’ll go to your house, whether you’re in Orlando or anywhere in Central Florida.

Does Home Insurance Cover Roof Shingles: File the Claim

Filing a claim for roof shingles doesn’t need to be a headache, unless you try to do everything in the dark. Let’s break it down into clear, simple steps so you don’t waste time or money.

- Check your policy first: Before calling anyone, review your homeowner’s insurance policy. Look for:

- Roof coverage terms (ACV or RCV).

- Exclusions (like age limits or wear and tear).

- Deductible amount.

- Time limits for filing claims.

- Take immediate photos: Snap everything, even the stuff that looks obvious. Overall roof damage, close-up of missing or cracked shingles, fallen shingles on the ground and inside damage (leaks, stains on the ceiling).

- Get a roof inspection from a licensed professional: Call a licensed roofing contractor in your area. Make sure the roofer provides:

- A detailed inspection report.

- Photos with damage highlights.

- Written estimate for repairs or replacement.

- File your claim with insurance: Now it’s time to make it official. Contact your insurance company or agent, submit your photos and roofer’s report, fill out the necessary claim forms and ask about timelines and what to expect next.

- Schedule the insurance adjuster visit: Your insurer will send an adjuster to inspect the damage, and you need to be present during the inspection, ask your roofer to be there too, this keeps things fair and don’t accept lowball estimates without question.

- Wait for the decision: After the inspection, you’ll get one of three responses:

| Result | What It Means |

| Approved | Your claim is accepted, payment is on the way. |

| Partially Approved | Some damage is covered, but not all. |

| Denied | You’ll get a letter explaining why. |

- Complete repairs and submit final docs: If your claim is approved, hire a licensed roofer to do the work, keep all receipts and “after” photos and submit proof to the insurer (especially if your policy includes RCV).

- Get the final payment: If your policy includes Recoverable Depreciation, you’ll get a second payment after submitting proof of completed work. No proof = no money. Simple as that.

Denied Claim for Roof Shingles? Here’s What You Can Do

Let’s walk through what you can do when your insurance denies your shingle roof claim.

- Read the denial letter carefully: Look for the exact reason for denial (wear and tear, improper maintenance, age, etc.), the policy sections referenced and the deadlines for appeal or reconsideration.

- Get a second opinion: Have a licensed roofing contractor like Protect Preserve Roofing inspect your roof and compare findings. Many homeowners in Orlando and Central Florida get their claims reversed after submitting a detailed second report.

- File a formal appeal: Yes, you can appeal, and you should if you believe the denial was unfair. Steps to follow:

- Write a formal appeal letter.

- Include your roofer’s second Opinion.

- Add any missing photos or receipts.

- Request a re-inspection, if possible.

- Involve a public adjuster: Still hitting a wall? Bring in a licensed public adjuster. They work for you, not the insurance company, reassess your claim with expertise and help negotiate a better settlement.

- File a complaint with Florida’s Department of financial services: If you live in Florida, you can report unfair treatment. The state may investigate the insurance company, pressure them to re-evaluate and assist you in getting fair treatment.

- Consider legal action: This is usually the last step, but in some cases, it’s the only way to force fair compensation, especially after hurricane or storm damage in Florida.

Still unsure what to do? Protect Preserve Roofing helps homeowners in Orlando and Central Florida navigate denied claims every week. We know how to document, defend and refile damage reports that meet insurer expectations.

Do All Insurance Companies Cover Shingle Roofs the Same Way?

Not even close. It might sound logical to think that all home insurance policies treat shingle roofs the same, but nope, they don’t. Each insurer has its own rules, limits and “fine print” that can make or break your claim.

Why coverage varies

Every insurance company evaluates risk differently. Here’s what changes from company to company:

- Policy type (HO-1, HO-3, etc.).

- Age limits on shingle roofs (some stop full coverage after 15 years).

- Deductible structure.

- Covered causes (some exclude wind or hail in specific zip codes).

- Replacement vs. repair decisions.

The “named perils” vs. “all-risk” factor

Some policies only cover specific causes of damage. These are called “Named Peril” policies. Others cover almost everything, unless it’s clearly excluded. These are “All-Risk” or “Open Peril” policies. Let’s take a look:

| Type of Policy | What It Means |

| Named Peril | Covers only listed events (wind, hail, fire, etc.) |

| All-Risk | Covers all damage unless specifically excluded |

Location… zip code?

Yep, where you live affects your coverage. In Florida, especially Central Florida, some companies:

- Exclude windstorm damage unless you buy extra coverage.

- Require stricter inspections for older roofs.

- Demand photos or proof of regular maintenance.

Not all roofs are treated equally

Here’s what some insurers look at before deciding your shingle claim:

- Roof material (asphalt shingles vs. metal).

- Pitch of the roof (flatter roofs sometimes cause disputes).

- Previous claim history.

- Photos from the initial inspection.

Quick reminder from Protect Preserve Roofing: Insurance companies don’t follow a single script. Your roof might be in great shape, but if your policy is strict, or outdated, you could still get denied. That’s why working with a licensed roofing professional who knows how to handle insurance language is your best move.

Shingle Materials Matter: Coverage Based on Roof Type

Not all shingles are treated equally by your insurance. In fact, the type of shingle on your roof can directly affect if your insurance will pay. We will analyze with the table below:

| Shingle Type | Lifespan | Insurance Viewpoint | Typical Coverage Limits |

| 3-tab Asphalt | 15–30 years | Most accepted | Often covered, but watch out after year 15 |

| Architectural | 25–40 years | Viewed as higher-end | Stronger coverage terms |

| Wood Shake | 20–30 years | Risky due to fire | Limited coverage in many areas |

| Metal Shingles | 40–70 years | High durability = insurer favorite | May lower premiums |

| Slate or Tile | 50+ years | Expensive to replace | May have payout caps or require add-ons |

Each material comes with different costs, wear patterns and risks – and insurance companies know that.

Why this matters for your claim

Insurers love numbers. When you file a claim, your roof material helps them calculate:

- How long your roof “should” last.

- Whether damage came from age or storm.

- How much your payout might be or if you’ll get denied.

Asphalt shingles are the standard, but they’re not a free pass

Most Florida homes have asphalt shingles. They’re affordable, easy to install and tough. But here’s the catch:

- After 10–15 years, your policy might shift from replacement cost value (RCV) to actual cash value (ACV).

- That means less money in your pocket.

- Some companies even stop full roof coverage once asphalt shingles reach a certain age.

Always check your policy. Age limits vary wildly.

Pro tip: Insurance loves maintenance. no matter the material, insurers love seeing that you’ve kept your roof in shape.

Emergency Roof Tarps

A roof tarp is a heavy-duty waterproof sheet installed over damaged areas of your roof to stop water from getting in. Simple, right? However, the right installation makes all the difference between protecting your home and causing even more damage.

Sure, it looks like a temporary band-aid. But here’s what many homeowners don’t realize:

- Insurance companies often require tarp installation to prevent further damage.

- If you don’t tarp your roof and water gets in, your claim could be denied.

- Improper tarp setup (like using nails or screws) can void parts of your coverage.

Protect Preserve Roofing uses sandbags and safe anchoring methods. We don’t pierce your roof unless it’s necessary (and even then, only in extreme cases such as a very high pitch or practically lost roof).

What emergency tarps actually protect you from

| Problem | Without a Tarp | With a Tarp |

| More water damage | Water seeps into insulation, walls, and furniture | Damage is halted immediately |

| Mold risk | Grows fast in Florida’s heat + humidity | Moisture is blocked |

| Insurance denial | “Negligence” may void part of your claim | Claim stays protected |

| Delays in repairs | Further damage means longer wait | Roof stays ready for inspection |

What does a tarp installation cost?

Tarp installations aren’t free and Protect Preserve Roofing is upfront about that. Expect prices between $800 and $1,600, depending on:

- How steep your roof is.

- How tall your home is.

- The size of the damage.

- Whether the area is safely accessible.

These prices follow our standard base, and they reflect quality, speed, and compliance with what insurers expect.

Conclusion: Protect Preserve Roofing — Serving Orlando & Central Florida with Trust

Now that you know the answer to “does home insurance cover roof shingles”, keep in mind that if your roof is leaking or your insurance claim feels like a headache waiting to happen, you don’t have to face it alone.

Protect Preserve Roofing isn’t just another name on a list. We’re licensed, insured and local. That means when the storm hits or your roof starts failing, we show up fast because we’re based right here in Orlando, and we serve Central Florida homeowners who need real help, not runaround.

Here’s what you can count on with us:

- Clear, upfront answers.

- Fast tarp installation with full insurance compliance.

- Support with filing your claim, the right way.

- Honest evaluations, licensed roof repairs and full replacements when needed.

Got roof trouble? Contact us now and:

- Schedule a clear, honest and free roof assessment.

- Call us directly, we actually pick up the phone.

- Get an instant roof estimate.

We know Florida roofs, speak insurance and most importantly… we’ve got your back.

Does home insurance cover roof shingles that blown off by wind?

Yes — if the damage was caused by a sudden event like strong wind or a storm. Most insurance policies include wind damage under covered perils. Wear and tear, however, is usually not covered.

Is there a difference between ACV and RCV in a roof claim?

Yes. ACV (Actual Cash Value) pays for the current depreciated value of your roof. RCV (Replacement Cost Value) pays for a full roof replacement without subtracting depreciation. The difference can be thousands of dollars.

Can I file a claim for just a few missing shingles?

You can, but approval depends on the severity of the damage. If a few shingles blew off but caused no interior damage, the claim might be denied or fall below your deductible.

Do I need emergency tarps while I wait for insurance?

If your roof was damaged in a storm and is leaking, installing an emergency tarp is considered “reasonable prevention”. Many Florida policies will reimburse this cost – as long as you save the receipt and use a licensed roofing company.

Leave a Reply