Roof replacement financing might seem overwhelming, but it doesn’t have to be. Whether your roof got wrecked in a storm or it’s simply reached the end of its life, figuring out how to pay for it shouldn’t be another stress on your plate.

According to HomeAdvisor, the average cost of a roof replacement in the U.S. ranges from $8,000 to over $15,000, and that number can climb fast depending on the size, pitch, and materials.

That’s why, in this guide, we’ll break it all down: the best ways to finance a roof replacement, what to watch out for in fine print, how your credit score, location, and roofing contractor affect your financing options and how Protect Preserve Roofing helps homeowners like you choose smart plans.

Don’t wait until a leak becomes a flood. The longer you delay, the worse (and more expensive) it gets. Let’s walk through your options so you can take action with clarity and confidence.

Can You Finance Roof Replacement? Here’s the Truth

Yes, you can finance a roof replacement and, in many cases, it’s the smartest move you can make.

A full roof replacement can cost anywhere from $8,000 to over $15,000, depending on the size of your home, materials used and how urgent the job is. Most homeowners in Orlando and Central Florida don’t have that kind of money sitting in the bank and that’s okay.

Financing gives you breathing room. It helps you fix the problem now and pay for it overtime without draining your savings or maxing out your credit card.

Why financing makes sense

Financing a new roof isn’t a luxury, it’s a smart way to protect your home. It means that you:

- Keep your home dry and secure.

- Avoid emergency costs from escalating damage.

- Spread payments over time in a manageable way.

- May even increase your property value.

This way, you’re not stuck with one lender or one payment plan. There are multiple ways to finance a roof replacement:

- Personal loans.

- Home equity loans or lines of credit (HELOCs).

- Government-backed loans (like FHA Title I).

- Roofing contractor financing with approved providers.

- 0% promotional credit card offers (for short-term needs).

Each option comes with pros and cons, and we’ll break those down next. However, the point is: you have options and none of them require upfront cash or perfect credit.

And don’t forget that Florida’s climate makes roof damage a serious issue. Between hurricanes, hail, and sun exposure, it’s not uncommon for homeowners to need roof work every 10 to 15 years. That’s why roof replacement financing in Orlando and surrounding areas is not just common, it’s practical.

Companies like Protect Preserve Roofing understand the urgency and provide financing guidance tailored to Central Florida residents.

How Much Does a Roof Replacement Really Cost?

Replacing a roof isn’t cheap. In 2025, the average cost to replace a roof in the U.S. ranges from $8,000 to $15,000, depending on several factors. If you live in Orlando or Central Florida, the range often falls between $8,500 and $14,000, with some jobs reaching higher due to hurricane prep codes. Let’s break down why.

What drives the price up

A roof isn’t just shingles. It’s a system and the final cost depends on what your house really needs. Here’s what affects your total:

- Size of the roof: Bigger roof, bigger price.

- Pitch (steepness): Steep roofs need more safety gear and labor time.

- Material used: Asphalt shingles are cheaper. Metal, tile or slate? Expect more.

- Structural damage: If there’s rot, mold or framing damage underneath, the price goes up.

- Permit requirements: In Florida, codes are strict. That adds paperwork, inspections and labor.

Real numbers, real examples

Let’s make it real. Here are typical price examples for homeowners in Central Florida:

| Roof Size | Material Type |

| $3.50 – $5.50 sq ft | Asphalt shingles |

| $4.50 – $7.50 sq ft | Architectural |

| $8.00 – $15.00 sq ft | Metal roofing |

| $10.00 – $18.00 sq ft | Tile roofing |

These prices include removal of old material, underlayment, ventilation, permits and labor, with no hidden surprises.

Florida-specific factors

Living in Florida means facing intense heat, hurricanes, and heavy rain. These affect both the roofing material you choose and how it must be installed to meet building codes. That adds cost, but also adds protection.

- Hurricane clips and reinforcements are required in many counties.

- Insurance requirements demand specific materials and installation techniques.

- Florida homeowners often pay more in the upfront but avoid costly repairs later.

Quick reminder: If you don’t understand the range, you can’t finance smartly. Some lenders require a detailed project estimate before approval. Protect Preserve Roofing provides transparent pricing, so you’re not caught off guard.

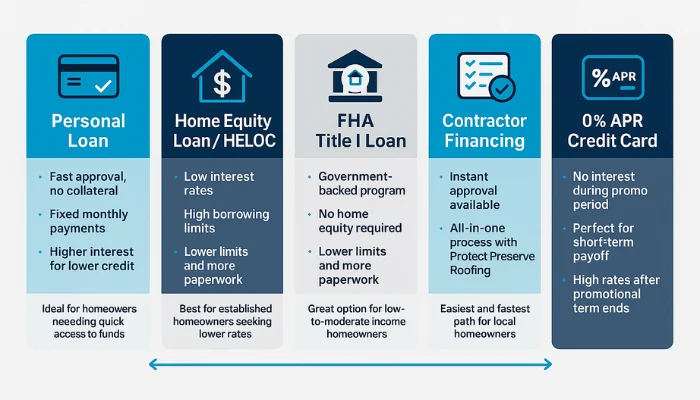

Roof Replacement Financing Options

There’s no one-size-fits-all solution when it comes to roof financing. Your credit score, home equity and urgency all play a role. So instead of guessing, let’s make things clear.

Here’s a simple table comparing the most popular financing options used by homeowners in Orlando and Central Florida:

| Financing Option | Ideal For | Pros | Cons |

| Personal Loan | Fast approval, decent credit | • Quick access to funds • Fixed payments | • Higher interest for low credit • No tax benefits |

| Home Equity Loan / HELOC | Homeowners with equity | • Lower interest • Higher limits • Possible tax deductions | • Requires equity • Risk of foreclosure • Longer process |

| FHA Title I Loan | Low-to-mid income homeowners, no equity | • Government-backed • No equity needed • Fair terms | • Smaller loan caps • More paperwork • Must use licensed contractor |

| Contractor Financing | Anyone looking for convenience | • Easy process • Fast approval • No separate lender needed | • Limited to what contractor offers • Always check full terms |

| 0% APR Credit Card | Small projects, short-term payoff ability | • No interest if paid on time • Immediate use | • High interest after promo • Requires strong credit |

Why Local Matters

In Orlando and Central Florida, building codes, permit fees and hurricane protection add unique costs. That’s why Protect Preserve Roofing works directly with financing providers who understand regional pricing and urgency. We help you:

- Choose the right plan based on your budget.

- Get approved quickly.

- Avoid predatory lending or bait-and-switch offers.

Pros and Cons of Financing a New Roof

Financing a roof isn’t just about getting the job done, it’s about doing it at the right time, without wrecking your savings or peace of mind.

Therefore, financing isn’t perfect for everyone. So, here’s a direct look at the benefits and trade-offs:

| Pros | Cons |

| Fix your roof immediately — no need to wait for savings | Interest costs — depending on terms, you’ll pay more over time |

| Flexible payment plans — break big costs into monthly chunks | Loan approval depends on credit — some plans need good credit |

| Avoid further damage — leaks and rot get expensive fast | Risk of overborrowing — taking more than you need adds pressure |

| Protects your home’s value — a new roof is an investment | Potential fees — watch out for origination or late fees |

| Access to better materials — don’t settle for cheap fix | Commitment — once approved, you’re locked into repayment |

Should you finance or pay out-of-pocket?

Ask yourself:

- Can I afford the full cost today without dipping into emergency funds?

- Will waiting to save more money cause bigger damage or insurance issues?

- Do I qualify for low-interest financing that won’t become a burden?

If the answer leans toward “I need the roof now, but can’t pay everything upfront,” then financing is worth considering.

Florida-specific reminder

In Florida, roof damage can spiral quickly, especially after storm season. Many insurance companies deny claims when they see “delayed action,” even if damage started from weather. Financing helps you act fast, protect your home and avoid bigger battles later.

Quick reminder: Want to see which plan fits your needs? Protect Preserve Roofing helps you compare offers and choose the one that fits your wallet, not someone else’s quota.

Which Roof Financing Option Fits Your Budget?

Choosing the right financing plan isn’t about picking the first option that pops up. It’s about making a move that fits your monthly income, your credit and the urgency of your roof issue.

Let’s walk through common financial situations and match each with the best roof replacement financing choice.

| Your Situation | Best Fit Financing Option | Why It Works |

| I need a roof now, and I have decent credit | Personal loan or Contractor financing | Quick approval, fixed payments, no equity required |

| I have home equity and want low interest | Home equity loan or HELOC | Lower rates, higher limits, possible tax advantages |

| I have low income and no equity | FHA Title I loan | Government-backed, fair terms, equity not required |

| I can pay it off quickly and have strong credit | 0% APR credit card | Zero interest if paid in promo period, immediate access |

| I don’t want to deal with banks or long processes | Roofing contractor financing (Protect Preserve) | All-in-one experience, fast answers, local support |

And here’s what to do before choosing:

- Get a full quote from your roofer. Know the real cost, not a ballpark.

- Check your credit score, it affects rates and approval.

- Decide how fast you can realistically pay it off.

- Ask about interest, fees and early payoff penalties. Every lender has different terms.

Key takeaway: The best roof replacement financing plan is the one you understand, trust and can stick with without stress.

How to Qualify for Roof Replacement Financing (Step-by-Step)

You don’t need to be a financial wizard to get approved for roof financing. Most lenders, and roofing companies that offer financing, want to work with you. The key is knowing what they’re looking for. Here’s how to make the process smooth and stress-free.

Step 1: Know your credit score

Your credit score is the first thing lenders check. Here’s a quick breakdown:

| Credit Score Range | Financing Type Likely Approved |

| 720 or above | Best rates, most lenders, no collateral |

| 640–719 | Good chance of approval, moderate rates |

| 580–639 | Limited options, higher interest rates |

| Below 580 | Tougher to qualify — FHA or co-signer may help |

Tip: You can check your score free through apps like Credit Karma or your bank’s website.

Step 2: Gather basic documents

Lenders will want to see proof you can pay back the loan. You’ll need:

- Valid ID (driver’s license or passport).

- Proof of income (pay stubs, W-2s, tax returns).

- Bank statements (last 1–3 months).

- Roofing estimate or project quote (from Protect Preserve Roofing, for example).

Step 3: Decide how much you need

Don’t guess. Use your contractor’s official quote to request the exact amount you’ll need, not more. Overborrowing can backfire and trigger higher monthly payments.

Protect Preserve Roofing provides detailed estimates that make lender approval easier and faster.

Step 4: Choose your financing path

Pick the plan that matches your financial situation:

- Good credit? Try a personal loan or credit union.

- Have equity? Look into a home equity loan or HELOC.

- No equity or lower income? Consider an FHA Title I loan.

- Want simplicity? Go with contractor financing, fast and handled in-house.

Step 5: Submit and wait (but not long)

Most applications take less than 5 minutes online. Some lenders give instant pre-approval. With roofing companies like Protect Preserve Roofing, you can get support during the application and help reading your offer before you sign.

Bonus tip: Watch the fine print

Always check:

- APR (interest rate).

- Term length (in months or years).

- Monthly payment.

- Early payoff penalties or hidden fees.

If it doesn’t make sense… ask. A good lender (or roofing partner) should explain every number.

Bottom line: Qualifying for financing isn’t hard. It’s just a checklist and with the right help, you don’t have to do it alone.

Roof Loans vs Insurance Claims: What’s the Difference?

Roof damage can catch you off guard and when it happens, most people ask the same question: “Can my insurance cover this, or do I need to get a loan?” The short answer? It depends on what caused the damage.

Here’s a breakdown to help you understand which path makes sense and what to do next:

| Feature | Insurance Claim | Roof Financing (Loan) |

| When It’s Used | Sudden damage from storms, hail, fire, fallen trees | Wear-and-tear, age, upgrades, partial replacements |

| Approval Time | Days to weeks (adjuster, paperwork, inspections) | Minutes to a few days, often faster with contractor help |

| Payment Structure | Lump sum (based on coverage and adjuster report) | Monthly payments over a set term |

| Out-of-Pocket Costs | Deductible required (varies by policy) | Depends on loan type and amount borrowed |

| Who Controls the Money | Insurance company (often pays roofer directly) | You or the roofer, depending on loan provider |

| Coverage Restrictions | Only covers qualifying damage | Covers anything you choose — full or partial roof |

The catch with insurance in Florida

In Florida, insurance companies are picky when it comes to roof claims. They often deny coverage if they believe:

- The damage was due to age, not a specific event.

- You waited too long to fix it.

- The roof wasn’t properly maintained.

Also, insurance usually doesn’t cover interior damage caused by leaks, unless you acted quickly and document everything. So, if water sat for days, that damage might come out of your pocket.

Can you use both?

Yes, in some cases. If insurance only pays for part of the repair or replacement, you can use financing to cover the gap. For example:

- Insurance pays $7,000

- Full replacement quote is $11,500

- You finance the remaining $4,500

Protect Preserve Roofing has helped dozens of Orlando homeowners combine both options smartly, without delays or confusion.

Bottom line: If your roof damage is sudden and covered, use insurance. If it’s wear, age or denied coverage, financing can step in fast. And if you need help sorting it out? That’s where we come in.

Conclusion: Local Roof Financing Support You Can Trust

If you’re living in Orlando or anywhere across Central Florida, your roof isn’t just protection, it’s peace of mind. And when something goes wrong, the last thing you need is confusion about how to pay for it.

That’s why Protect Preserve Roofing is here, not just to install a quality roof, but to make the process affordable, local and clear from the first call to the final nail.

We don’t send out generic forms or give you the runaround. We work with trusted roof replacement financing providers and walk you through every option, from interest promotions to extended low payment plans all based on your needs, not some template.

Ready to talk? If your roof needs help and your budget needs options, let’s connect. Just:

- Schedule a clear, honest and free roof assessment.

- Call us directly, we actually pick up the phone.

- Get an instant roof estimate.

We’ll give you the honest truth, a fair quote and financing that fits your life. Let’s protect your home the right way.

Can I finance a roof replacement with bad credit?

Yes, but your options may be limited. Some lenders offer plans for credit scores below 600, but interest rates are usually higher. FHA Title I loans and contractor financing (like what Protect Preserve Roofing offers) can be more flexible.

Does roof financing cover everything, including labor and materials?

Yes. Most financing options are designed to cover the full cost, including materials, labor, permits, and any extras included in your roofing quote.

How do I know what my roof will really cost?

We’ll come to your home and give you a full, written quote — free of charge.

No guessing, no vague ranges. Just real numbers so you can finance the right amount from the start.

Is financing available for commercial roofing too?

Yes. Financing is available for residential and commercial roofing in most cases. Terms may vary depending on the size of the project and credit profile.

Leave a Reply